Relm publishes research-led insights exploring financial literacy, behavioural science, and financial decision-making. Our work examines how individuals interact with financial systems, the behavioural barriers that shape outcomes, and how policy and programme design can be improved using behavioural evidence.

Our publications combine behavioural economics, psychology, and policy analysis to inform organisations, policymakers, and practitioners working to improve financial wellbeing.

We publish:

• Research insights on financial literacy and behavioural science

• Policy commentary on UK financial wellbeing initiatives

• Behavioural analysis of financial decision-making

• Evidence-informed recommendations for programme design

• Thought leadership pieces shaping future research agendas

Upcoming outputs will include policy briefs, research reports, and commissioned studies evaluating financial literacy programmes and behavioural interventions.

For collaboration or commissioned research, please contact Relm directly.

Recent Publications

What if Financial Systems Were Designed for How People Actually Think?

Financial systems are often designed under the quiet assumption that individuals make rational decisions, carefully weighing options, comparing costs and selecting the optimal choice that serves their long-term interests. In an ideal world, this theory seems reasonable; however , in practice, financial decisions are rarely made under ideal conditions. People make financial decisions when they…

Why financial literacy needs behavioural science

Moving from Information to Decision-making Financial literacy has been positioned as the cornerstone of financial wellbeing for some time now. Schools, Governments, financial institutions and charities invest heavily in programmes designed to improve understanding of financial concepts such as spending, budgeting, saving and investing. The underlying assumption here being that once knowledge obtained and understood,…

Why knowing more about money still isn’t enough

Rethinking Financial Literacy Through Behavioural Science Financial literacy has been a central focus of policy and education for decades. The dominant narrative is something along the lines of: if individuals are given the right information – about budgeting, saving, debt or investing – then they will make better financial decisions. Schools, banks, nonprofits and governments…

Enter the Relm of Change

About Relm Relm is an applied research and advisory initiative focused on improving financial decision-making through behavioural science. At its core, Relm exists to address a persistent gap:while access to financial services has expanded and financial education has improved, many individuals still struggle to make decisions that support their long-term financial wellbeing. This gap is…

Frameworks

Relm has researched and developed several frameworks that inform our reviews, analysis and research. Our most recent publications have introduced our:

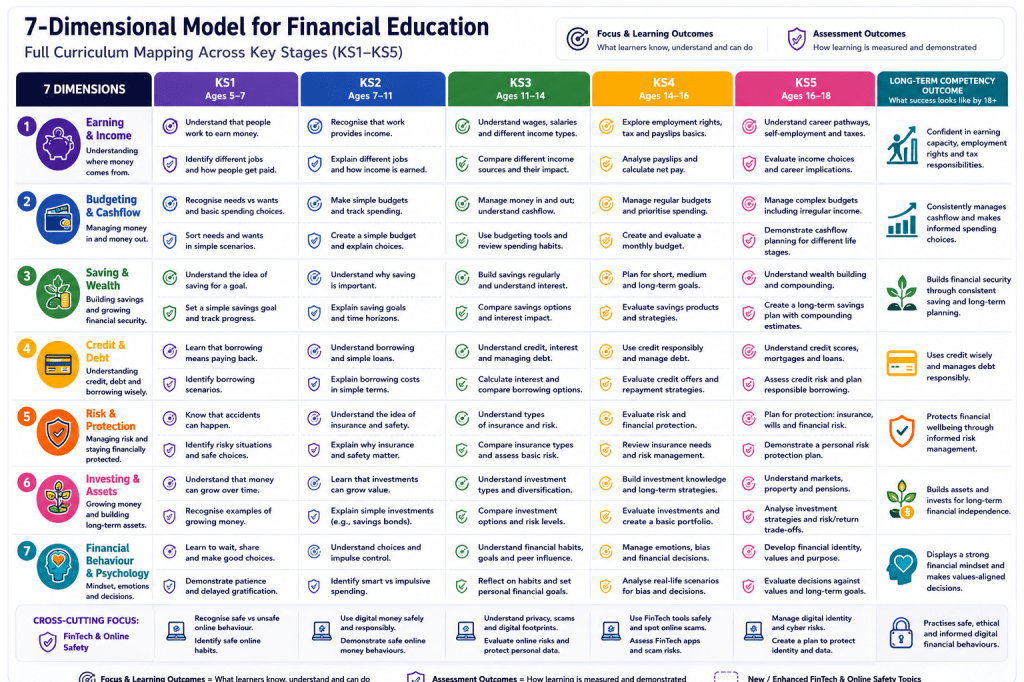

• 7-Dimensional Model for Financial Education

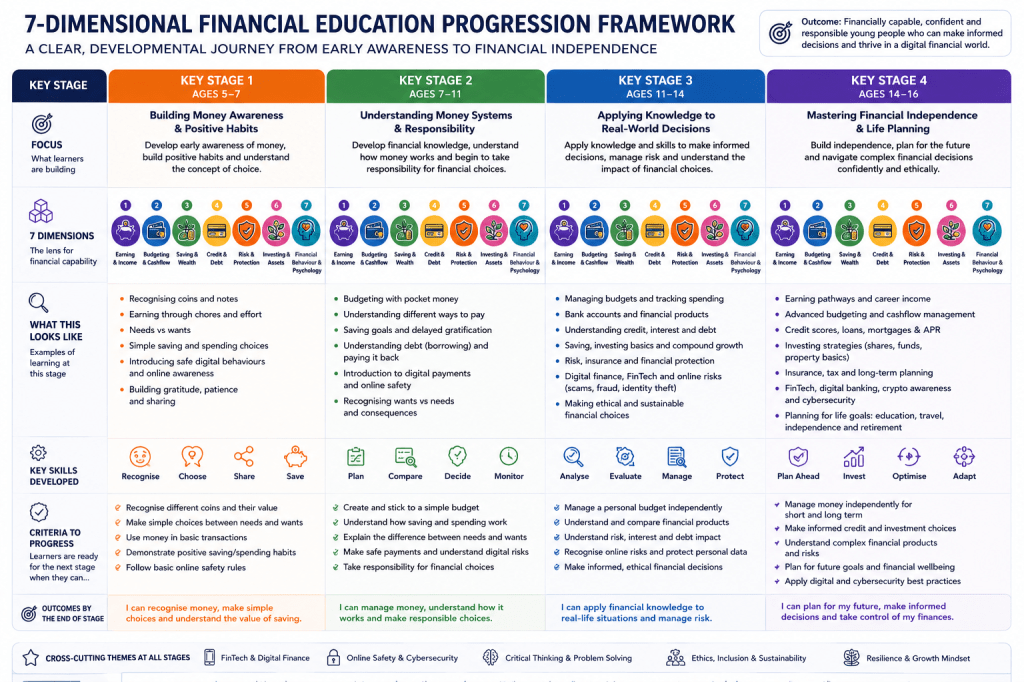

• 7-Dimensional Progression Model.

•Behavioural Drivers Model (BDM)

These frameworks act as the national cirriculum architechture that can be used to guide programme designers, schools and policymakers – where each framework integrates horizontally or vertically into each other to create a financial capability framework.

Below are the following frameworks. For more details or if you would like to adpot/integrate these frameworks, please get in touch via our contact page.

7-Dimensional Model for Financial Education

The model is structured across seven interdependent dimensions:

Foundational Financial Knowledge

Core concepts such as money, value, income, expenditure, credit, taxation, and inflation.

Financial Decision-Making and Behaviour

Day-to-day financial choices, budgeting, saving, spending prioritisation, and opportunity cost reasoning.

Economic Understanding and Systems Thinking

Understanding how economies function, including markets, employment, interest rates, and economic cycles.

Risk, Credit, and Financial Protection

Credit use, debt management, insurance, fraud awareness, and financial risk evaluation.

Digital and Modern Financial Capability

Digital banking, fintech systems, online transactions, data privacy, and emerging financial technologies.

Psychological and Behavioural Finance

Cognitive biases, emotional decision-making, impulse control, financial identity, and behavioural self-regulation.

Financial Citizenship and Life Planning

Long-term planning, wealth building, ethical financial behaviour, sustainability, and intergenerational responsibility.

Collectively, these dimensions ensure that financial education is not reduced to numeracy or budgeting alone, but instead reflects the complexity of real-world financial life.

7-Dimensional Progression Model

The progression model is structured as follows:

Stage 1: Emergent Awareness – Recognising money and basic exchange concepts

Stage 2: Guided Application – Performing structured financial tasks with support (e.g., saving, simple budgeting)

Stage 3: Functional Independence – Managing routine financial decisions with limited guidance

Stage 4: Applied Understanding – Understanding consequences, trade-offs, and financial planning

Stage 5: Strategic Behaviour – Long-term planning, credit use, and risk evaluation

Stage 6: Adaptive Financial Capability – Adjusting behaviour across contexts, income variability, and financial systems

Stage 7: Financial Maturity and Citizenship – Autonomous, ethical, and system-aware financial decision-making with long-term intergenerational awareness

Each of the seven curriculum dimensions is mapped across these progression stages, ensuring that learning is both vertically coherent (within a domain) and horizontally integrated (across domains). PLEASE NOTE: We are aware that the progression model does not include Key Stage 5 and we are working to amend this.

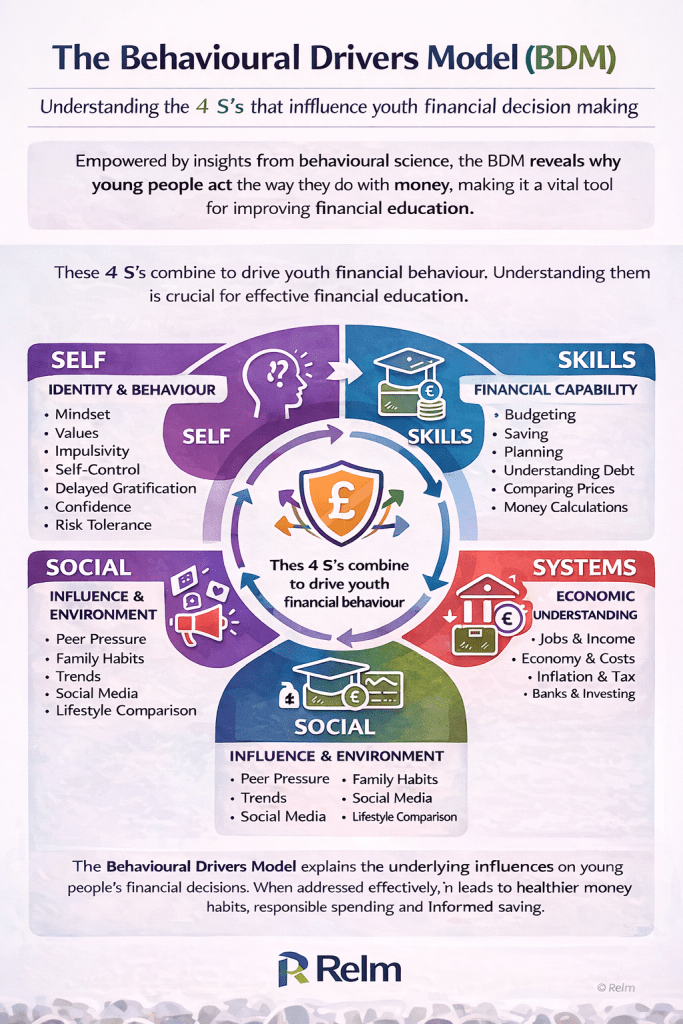

The Behavioural Drivers Model (BDM)